Legal Scrutiny Report (LSR) in Banking: Nature, Scope, and Legal Position

In secured lending transactions involving immovable property, banks rely on a Legal Scrutiny Report to verify title, marketability, and enforceability of the security. An analysis of the statutory framework, the scope of advocate verification, and the role of the LSR at the stage of enforcement.

Introduction

In secured lending transactions involving immovable property, banks and financial institutions undertake a process of legal due diligence through what is commonly termed as a Legal Scrutiny Report (LSR). The report is prepared by an advocate upon examination of title documents and allied records, with the objective of forming a legal opinion on the ownership, marketability, and enforceability of the security proposed to be created. The exercise is document-centric and forms an essential part of pre-sanction verification in banking transactions.

Statutory Framework Governing LSR

Although the LSR itself is not codified under a single statute, its foundation lies in the legal regime governing transfer, registration, stamping, and enforcement of security interests. The creation of mortgage and transferability of property are governed by the Transfer of Property Act, 1882. Registration requirements and public notice of transactions affecting immovable property are governed by the Registration Act, 1908. The admissibility and validity of instruments are subject to the provisions of the Indian Stamp Act, 1899.

In cases involving corporate borrowers, registration of charge assumes significance under the Companies Act, 2013. The enforcement of secured assets by banks and financial institutions is governed by the SARFAESI Act, 2002. Additionally, regulatory oversight and due diligence expectations are shaped by guidelines issued by the Reserve Bank of India.

Examination of Title and Ownership

The core component of an LSR lies in verification of title. The advocate is required to examine the chain of title for a reasonable period, ordinarily extending to several decades, to ensure continuity and absence of defects. Each transfer forming part of the chain is examined to ascertain whether it is supported by a valid and legally enforceable instrument.

The mode of acquisition is relevant in determining the strength of title. Where ownership is derived through succession, the scrutiny extends to verification of devolution of interest through legally recognised means. Any break, inconsistency, or absence of supporting documentation within the title chain may affect the conclusion regarding marketability.

Encumbrances and Third-Party Interests

A significant aspect of legal scrutiny involves determining whether the property is free from encumbrances. This requires examination of records maintained under the Registration Act, 1908 to identify any subsisting mortgages, charges, leases, or other third-party rights.

In the case of corporate entities, the existence of registered charges under the Companies Act, 2013 is examined, as it directly impacts priority of claims. The sufficiency of stamp duty under the Indian Stamp Act, 1899 is also relevant, since inadequately stamped instruments may not be enforceable in evidence.

Nature of Property and Statutory Compliance

The advocate is required to examine the nature and classification of the property, including whether it is freehold or leasehold, and whether its use complies with applicable land and municipal laws. Restrictions on transfer, if any, arising from local land laws or conditions of allotment, are required to be identified.

Revenue records, including mutation entries and land registers, are examined to verify possession and to ensure consistency with title documents. Discrepancies between documentary title and revenue entries may raise questions requiring clarification prior to creation of security.

Litigation and Legal Impediments

The existence of pending litigation, injunctions, or statutory proceedings affecting the property is a material consideration in legal scrutiny. Any ongoing dispute may impact the lender's ability to enforce security and therefore forms part of the advocate's examination.

Even in the absence of a registered encumbrance, a subsisting dispute or adverse claim may render the title doubtful from a legal standpoint. The advocate is required to assess whether such factors create a legal impediment to mortgage or enforcement.

Legal Opinion and Risk Assessment

Upon completion of scrutiny, the advocate furnishes a reasoned legal opinion indicating whether the title is clear, marketable, and capable of being mortgaged. Where defects or risks are identified, the opinion records the nature of such deficiencies and, where applicable, conditions subject to which the risk may be mitigated.

The LSR is advisory in nature; however, it constitutes a foundational document for the lender's decision to proceed with the transaction.

Relevance at the Stage of Enforcement

The adequacy of legal scrutiny assumes significance at the stage of enforcement under the SARFAESI Act, 2002. Any defect in title or irregularity in creation of mortgage may affect the enforceability of security interest and recovery proceedings initiated by the lender.

Conclusion

A Legal Scrutiny Report is integral to secured lending transactions involving immovable property. It entails a detailed legal examination of title, encumbrances, statutory compliance, and potential risks associated with the property offered as collateral. The exercise is inherently fact-specific and must be undertaken with reference to applicable laws and records.

Note

This article is intended for general informational purposes only and does not constitute legal advice or solicitation, in accordance with the Bar Council of India Rules.

More Insights

Legal Due Diligence in Real Estate Transactions in Bangalore

Bangalore's real estate sector is governed by a layered framework of central and state legislations. A comprehensive guide to title verification, RERA compliance, encumbrance checks, and the essential documents every buyer must examine before acquisition.

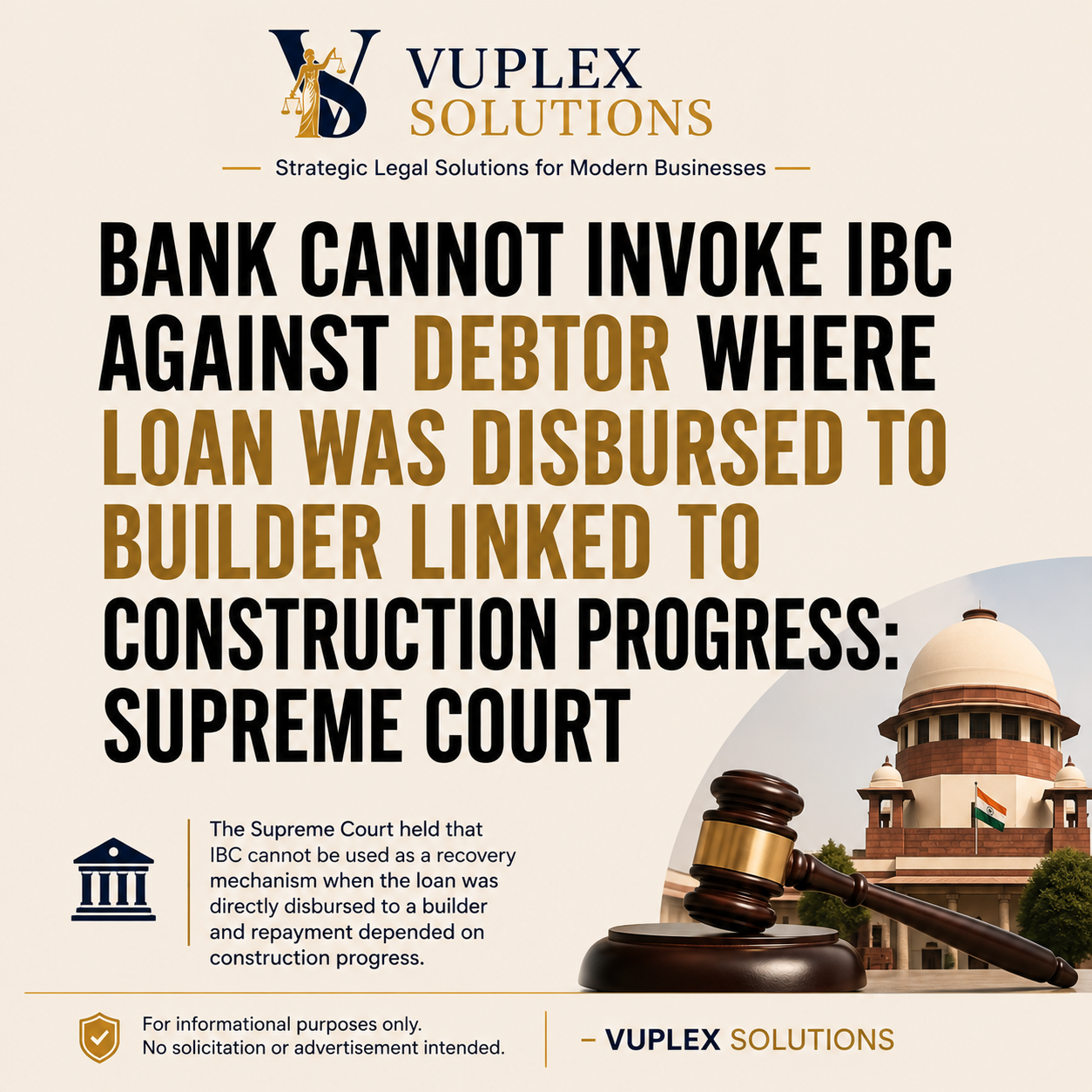

IBC Cannot Be Invoked as a Recovery Tool Where Loan Structure Is Performance-Linked: Supreme Court

The Supreme Court has reaffirmed that the Insolvency and Bankruptcy Code, 2016 is not a substitute for debt recovery, particularly where the underlying transaction involves performance-linked construction obligations and third-party disbursement.

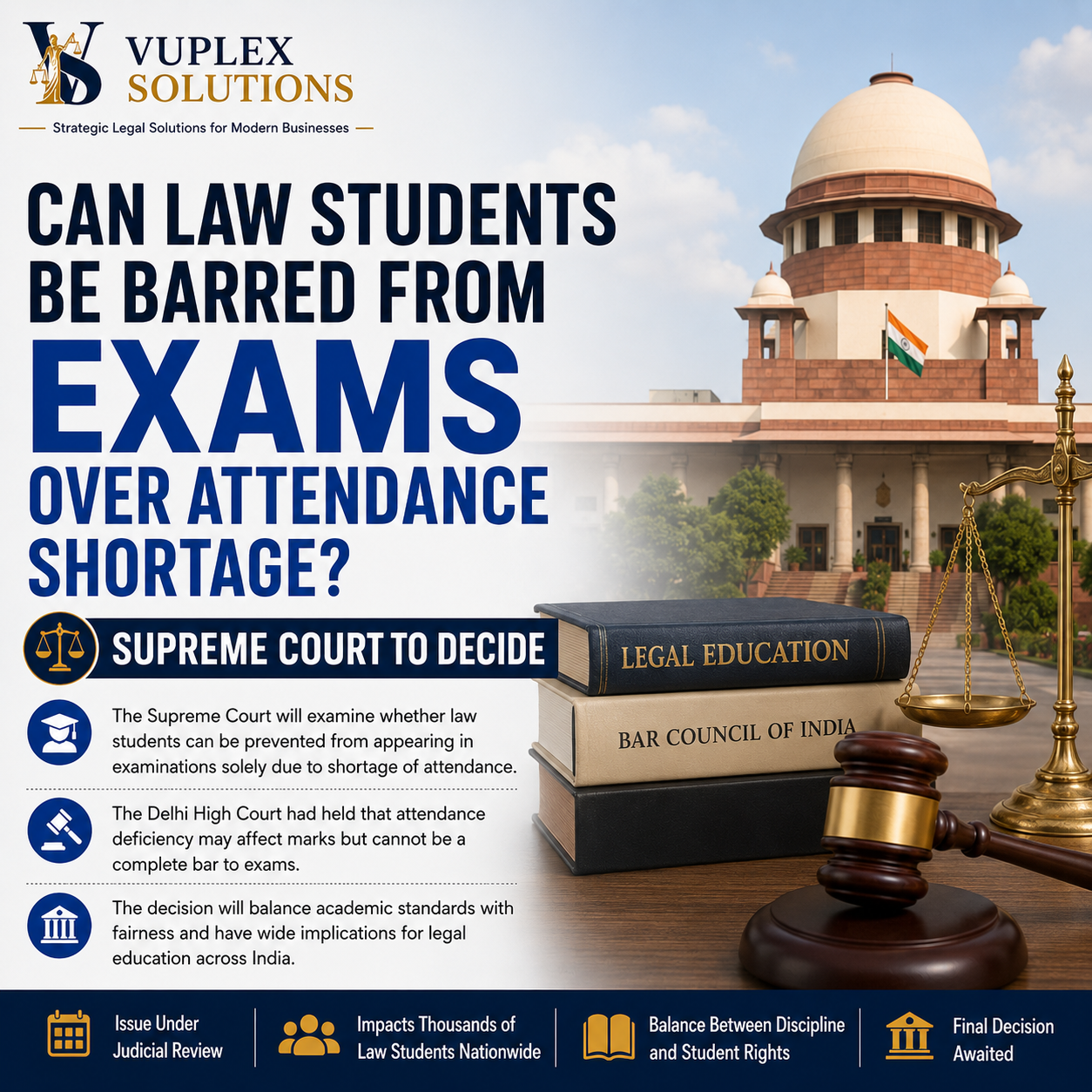

Can Law Students Be Barred From Exams Over Attendance Shortage? Supreme Court Set To Decide

The Supreme Court has agreed to examine the Delhi High Court's 2025 ruling that law students should not be detained from examinations merely for attendance shortage. A look at the competing considerations of academic discipline and proportionality.